Home

/ How To Calculate Bad Debt Expense : In the percentage of the outstanding debtor, a certain percentage of debtors is recorded as bad debt expense based on their aging or in simple word based on how old debtors are.

How To Calculate Bad Debt Expense : In the percentage of the outstanding debtor, a certain percentage of debtors is recorded as bad debt expense based on their aging or in simple word based on how old debtors are.

How To Calculate Bad Debt Expense : In the percentage of the outstanding debtor, a certain percentage of debtors is recorded as bad debt expense based on their aging or in simple word based on how old debtors are.. Under this approach, businesses find the estimated value of bad debt by calculating bad debts as a percentage of the outstanding accounts receivable balance. The formula uses historical data from previous bad debts to calculate your percentage of bad debts based on your total credit sales in a given accounting period. Percentage of credit sales method. Bad debts expense is also referred to as uncollectible accounts expense or doubtful accounts expense. The method consists of dividing the total amount of bad debt by the total accounts receivable for a given period.

In this example, estimated bad debts are $5,000. To record the bad debt expenses, you must debit bad debt expenses and a credit allowance for doubtful accounts. Bad debts expense results because a company delivered goods or services on credit and the customer did not pay the amount owed. Enter your basis in the bad debt in column (e) and enter zero in column (d). These types of questions are asked many times in the examinations of b com, ca, icma, icmai, cpa etc.

Percentage Of Sales Method For Estimating Bad Debt Expense Youtube from i.ytimg.com In the latter, you notate bad debt expenses as an ongoing cost of doing business. However, you also have to calculate bad debt expenses as business credit losses. The customer is given a specific period of time to repay this debt. How to calculate bad debt expense? In modern times, many goods and services are sold to customers on a credit basis. For example, if a company sells a total of $100 million worth of products on credit during a certain year, and $3 million of this amount turns out to be uncollectible. Enter your basis in the bad debt in column (e) and enter zero in column (d). The table below shows how a company would utilize the accounts receivable aging method to estimate bad debts.

For example, if a company sells a total of $100 million worth of products on credit during a certain year, and $3 million of this amount turns out to be uncollectible.

Percentage of bad debt = total bad debts / total credit sales Once the company determines the percentage, they multiply by the total credit sales to estimate the bad debt expense. To estimate bad debts using the allowance method, you can use the bad debt formula. In addition, this accounting process prevents the large swings in operating results when uncollectible accounts are written off directly as bad debt expenses. Calculating bad debt expenses businesses follow 2 methods of calculating bad debt expenses: Formula to calculate bad debt expense. Bad debts expense is also referred to as uncollectible accounts expense or doubtful accounts expense. Unlike the sales approach, the balance in the allowance. How to calculate bad debt expense with accounts receivable. The customer is given a specific period of time to repay this debt. In the latter, you notate bad debt expenses as an ongoing cost of doing business. For example, if a company sells a total of $100 million worth of products on credit during a certain year, and $3 million of this amount turns out to be uncollectible. Bad debt expense also helps companies identify which customers default on payments more often than others.

Percentage of bad debt = total bad debts / total credit sales To record the bad debt expenses, you must debit bad debt expenses and a credit allowance for doubtful accounts. Bad debt expense is reported on the income statement. The following formula is used to calculate a bad debt expense. How to calculate bad debt using the percentage of accounts receivable method:

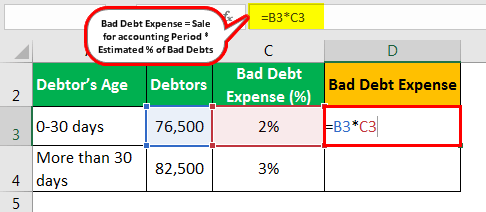

Accounts Receivable Bad Debt Expense Direct Write Off Method Vs Allowance Method Youtube from i.ytimg.com How to calculate bad debt expense with accounts receivable. The estimated percentages are then multiplied by the total amount of receivables in that date range and added together to calculate the amount of bad debt expense. Also, the company may use either net sales or credit sales during the year to calculate the bad debt expense. The formula uses historical data from previous bad debts to calculate your percentage of bad debts based on your total credit sales in a given accounting period. Estimating your bad debts usually involves some form of the percentage of bad debt formula, which is just your past bad debts divided by your past credit sales. For example, the company will record 1% as bad debts from debtors, which are not older than 30 days and 2.5% from debtors, which are not older than 60 days. So, the following exercise will help you greatly in mastering this topic. Unlike the sales approach, the balance in the allowance.

The bad debt expense formula.

You can compute your bad debts with this formula, where your previous bad debts are divided by your last credit sales. The bad debt estimate would be $6,250 (.025 x $250,000). It's subject to the capital loss limitations. The table below shows how a company would utilize the accounts receivable aging method to estimate bad debts. When it becomes apparent that a specific customer invoice will not be paid, the amount of the invoice is charged directly to bad debt expense. Once the company determines the percentage, they multiply by the total credit sales to estimate the bad debt expense. The bad debt expense formula. In modern times, many goods and services are sold to customers on a credit basis. Estimating your bad debts usually involves some form of the percentage of bad debt formula, which is just your past bad debts divided by your past credit sales. For example, the company will record 1% as bad debts from debtors, which are not older than 30 days and 2.5% from debtors, which are not older than 60 days. How to calculate bad debt expense? How to calculate bad debt expense with accounts receivable. However, you also have to calculate bad debt expenses as business credit losses.

In the former method, you record the specific bad debt expenses; How to calculate bad debt expense with accounts receivable; How to calculate bad debt expense with accounts receivable. Bad debt expense is reported on the income statement. Some companies estimate bad debts as a percentage of credit sales.

Bad Debt Expense Formula How To Calculate Examples from cdn.wallstreetmojo.com In modern times, many goods and services are sold to customers on a credit basis. Bad debts expense results because a company delivered goods or services on credit and the customer did not pay the amount owed. Some companies estimate bad debts as a percentage of credit sales. How to calculate bad debt expense? In the percentage of the outstanding debtor, a certain percentage of debtors is recorded as bad debt expense based on their aging or in simple word based on how old debtors are. However, you also have to calculate bad debt expenses as business credit losses. The bad debt estimate would be $6,250 (.025 x $250,000). The estimated percentages are then multiplied by the total amount of receivables in that date range and added together to calculate the amount of bad debt expense.

The customer is given a specific period of time to repay this debt.

Percentage of bad debt = total bad debts/total credit sales When it becomes apparent that a specific customer invoice will not be paid, the amount of the invoice is charged directly to bad debt expense. How to calculate bad debt expense with accounts receivable. The customer is given a specific period of time to repay this debt. Enter the name of the debtor and bad debt statement attached in column (a). The bad debt estimate would be $6,250 (.025 x $250,000). Either net sales or credit sales can be used for the calculation of bad debts. In this example, estimated bad debts are $5,000. It's subject to the capital loss limitations. The bad debt formula you will always count your allowance for bad debts because they are esteemed before the actual bad debts happened. This means that goods or services are provided to the customer now and then paid by the buyer at a future date. If the account has an existing credit balance of $400, the adjusting entry includes a $4,600 debit to bad debts expense and a $4,600 credit to allowance for bad debts. This is a debit to the bad debt expense account and a credit to the accounts receivable account.